Let’s say you’re at a local convention and you see the Barbie or GI Joe you used to have. It’s in its original box and it has a crazy-high price tag. You think to yourself, “If I kept just a few of my old toys in their original boxes, they could be worth hundreds now”. Well, here’s your chance to protect your POP! figs so they’ll be in mint condition 30 years from now. BCW offers clear boxes to protect POP! figs in their original box. Yes! A box in a protective box makes sense after you see the value of those familiar old toys.

Large and Regular Scale Pop Figures in Storage Boxes

BCW POP! Figure Boxes are made from PET (polyethylene terephthalate), an archival-quality, crystal-clear plastic that is semi-rigid and impact resistant. BCW offers protective boxes for the standard 4-inch figs and the larger 6-inch figs. Do not confuse these large figs with the even larger “vehicles”.

The article below by Artie Zillante is a pre-published draft of the paper. The final paper was published as a book chapter in 2008, in the Business of Sports (Volume 3), edited by Brad Humphreys and Dennis Howard.

by Artie Zillante University of North Carolina Charlotte November 25th, 2007

1 Introduction

If the attempt by The Upper Deck Company (Upper Deck) to purchase The Topps Company, Inc. (Topps) is successful, the baseball card industry will have come full circle in under 30 years. A legal ruling broke the Topps monopoly in the industry in 1981, but by 2007 the industry had experienced a boom and bust cycle1 that led to the entry and exit of a number of firms, numerous innovations, and changes in competitive practices. If successful, Upper Deck’s purchase of Topps will return the industry to a monopoly. The goal of this piece is to look at how secondary market forces have shaped primary market behavior in two ways. First, in the innovations produced as competition between manufacturers intensified. Second, in the change in how manufacturers competed. Traditional economic analysis assumes competition along one dimension, such as Cournot quantity competition or Bertrand price competition, with little consideration of whether or not the choice of competitive strategy changes. Thus, the focus will be on the suggested retail price (SRP) of cards as well as on the timing of product releases in the industry.

Baseball cards have undergone dramatic changes in the past half century as the industry and the hobby have matured, but the last 20 years have provided a dramatic change in the types of products being produced. Prior to World War II, baseball cards were primarily used as premiums or advertising tools for tobacco and candy products. Information on the use of baseball cards as advertising tools in the tobacco and candy industries prior to World War II can be obtained from a number of different sources, including Kirk (1990) and most of the annual comprehensive baseball card price guides produced by Beckett publishing. A discussion of the early secondary market is discussed by George Vrechek and can be found in 7 installments of Sports Collector’s Digest (SCD) in 2004 and 2005.2 The baseball card industry is typically defined as the producers of nationally distributed picture cards of major league baseball players, licensed by Major League Baseball (MLB) and either the Major League Baseball Players Association (MLBPA) or the individual major league baseball players. Since firms must be granted licenses by MLB and the MLBPA to produce cards that appeal to collectors on a national basis, entry into the industry is regulated by those two entities. As for the general terms of the license, MLB has a standard royalty rate of 11% for national retail product licenses, as well as minimum annual guarantees which vary depending on the different product classification. The MLBPA has similar requirements. According to O’Shei (1997b), the MLBPA also has to approve the final product, and will oftentimes make suggestions to the manufacturers about the design and price of the product. Note that not all manufacturers secure licenses from both sources — one manufacturer, Michael Schechter Associates (MSA) has never acquired a national license from MLB. MSA has acquired licenses from the MLBPA, airbrushing any part of the team logos on the players’ uniforms that appear in the picture so as not to infringe on any of MLB’s trademarks. However, these cards are not fully embraced by consumers, in part because they tend to be regional issues and in part because they lack the MLB logo of the player’s team.

Baseball cards are sold to consumers in retail outlets, such as Wal-Mart or Target, as well as in hobby shops. Card manufacturers are typically prohibited in their licensing agreements from selling directly to final consumers, so they sell cases of cards to the retail outlets, major hobby dealers, and wholesalers. Cases are comprised of a fixed number of boxes of cards, although the number of boxes varies depending on the manufacturer and brand of the product. Boxes of cards may be sold by the wholesalers to smaller hobby stores, or by retail chains and hobby stores to consumers. Boxes of cards are made up of packs of cards. Packs are the smallest packaged individual unit that a consumer can buy. Packs consist of the individual cards of a particular brand, and may contain any number of different types of cards.

Base cards comprise the bulk of the pack and make up the base set of the brand. A set of cards is determined by the brand name given to the cards made available in a pack by the manufacturer and by the manufacturer’s checklist for that brand. Insert cards are cards available in packs at a lower rate than base cards, often with a completely different design than the base cards in the set. Most insert cards are part of a small insert set, which is theme based and may include baseball all-stars, rookie prospects, or even the favorite players of the owner of the manufacturing company. A parallel card is a type of insert card that is identical to a base card from a brand except for some change in the border, lettering, or glossiness of the base cards in the pack. Parallel cards are usually inserted at a lower rate than regular base cards. Other types of insert cards will be discussed as needed within the following sections.

Manufacturers release brands throughout the course of the year. Many brands are released in a single series, but some are released in multiple series. Typically, the packs from one series do not contain the cards available in another series. Given that manufacturers now produce multiple brands, the “flagship” brand of a manufacturer is the one that bears the manufacturer’s name. For instance, the Topps Company produces both the Topps brand and the Stadium Club brand.3 The Topps brand is considered the flagship brand. The survival of remaining brands depends on their ability to fill a market niche. As former Topps employee Marty Appel states in Portantiere (1996):

“You hear people say there’s too much stuff being produced, that it’s too confusing, and to a large degree it’s true. However, Topps feels that if you have a message behind each product, like we do, you should be successful”.

A similar statement is made in Topps’ annual reports, as one of Topps’ goal is “to ensure that each brand of sports card has its own unique positioning in the marketplace”. Thus the theme and design of the brand can be viewed as defining the brand, as well as most of the innovation in producing a new brand.

The actual production of baseball cards is a fairly simple process for most types of cards. The principle steps are photographing the players, developing the brand’s theme, designing the cards, obtaining the statistics and text necessary for the card backs, the physical production of the cards, and shipment from manufacturer to wholesaler or retailer. Most of these processes are easily understandable, and, once the technology to produce the cards is in place, the most difficult part of the process is developing the brand’s theme. Topps’ website, www.topps.com, reports that the process of producing a set, from inception to shipment, is about six months. Upper Deck provides a slightly longer estimate, saying that the entire process of developing a brand takes about forty weeks. However, Upper Deck also states that the printing of the cards takes about one week.4

What follows is a description of the changes that have occurred in the baseball card industry in the past 60 years. The 60 years are broken into three time periods: the Pre-Fleer v. Topps Ruling era (1948-1980), Between the Strikes (1981-1994), and Product Proliferation and Industry Consolidation (1995-2006). In each of these time periods the major innovations in trading cards are discussed along with changes in competitive practices.

1This boom and bust cycle is detailed in Ambrosius (2002). 2This is also available online at http://www.oldbaseball.com/refs/1930s.htm. 3To distinguish between brands and manufacturers any time a brand is referenced it will be italicized. Thus, Topps refers to the manufacturer while Topps refers to the flagship brand of Topps. 4This length of time was provided in Geschke (1996). In Anon (2007), Topps reports that the process takes 30 weeks while Upper Deck reports a 6 month time frame.

2 Pre-Fleer v. Topps Ruling, 1948-1980

2.1 Early Competition (1948-1955)

Following the lead of earlier industries, Bowman Gum Company (Bowman) issued the first set of post-war baseball cards in attempt to boost sales of chewing gum in 1948. Prior to WWII, The Gum Inc. Co., an earlier company of Jacob Bowman, had issued cards under the name Play Ball. The Leaf Gum Company (Leaf) followed Bowman and produced a set in 1949. While Leaf discontinued production after one year, Bowman produced card sets from 1948 to 1955, at which time the company was purchased by Topps.5 Topps first produced a card set in 1951, although it was more a game than what would now be considered a traditional set of picture cards. In 1952 Topps produced its first “true” set, and competed head-to-head with Bowman for four years. After Topps’ purchase of Bowman in 1955, the company held a virtual monopoly in the sale and production of cards depicting current major league baseball players for the next 25 years.

During this time Topps and Bowman signed players to individual contracts. The specifics of the contracts varied depending on the player under contract and violations of contracts were debated in court.6 In 1952 the Topps and Bowman sets had 221 players in common. By 1953 the total was down to 115, in 1954 the total players in common fell to 84, and by 1955 it was down to 44. Part of this may have been due to player selection, but exclusive contracts were beginning to be used by the manufacturers and enforced by the courts. A famous example is the 1954 Bowman card of Ted Williams. Williams was under exclusive contract with Topps, and ultimately the Williams card in 1954 Bowman was replaced with Jimmy Piersall.

Given that the manufacturers were signing some players to exclusive contracts and that some players did not sign contracts with either manufacturer,7 neither manufacturer could produce a set of cards that included all major league players. Topps’ largest set during this time was 407 cards in 1952 and the set size would decrease each year, with a low of 206 cards in its 1955 set. Bowman’s set size had no discernible pattern as its smallest set was 160 cards in 1953 while its largest set was 320 cards in 1955. The 1953 set was issued in two series, one in color and the other in black and white. Although no citation confirms this, hobby lore has it that the black and white series was produced due to lack of funds to produce a second color series. In addition to competing for player contracts, competition is evident in pack prices during this time. Bowman had been charging a penny per card in a pack, but Topps packaged six cards for a nickel. Bowman subsequently increased the amount of cards in its nickel packs to seven in 1954 and nine in 1955 while Topps remained at six.

5Topps has changed its legal name multiple times in the past 50 years. Bowman was technically purchased by the Topps Chewing Gum Company. 6See Bowman Gum, Inc. v. Topps Chewing Gum, Inc., March 31, 1952 and Haelan Laboratories, Inc. v. Topps Chewing Gum Co., May 25, 1953. 7Stan Musial, who is generally regarded as one of the top 20 baseball players of all time and was a well-established veteran by the mid-50s, did not appear in either Bowman or Topps in 1954 and 1955.

2.2 Topps’ Monopoly Years (1956-1980)

From 1956-1980 Topps had a virtual monopoly on producing baseball cards with active players. Topps’ primary competitor was the Fleer Corporation (Fleer); however, since Topps had exclusive licenses with most of the players in major league baseball, Fleer did not provide much competition. Topps would obtain these exclusive licenses by signing prospects while they were in the minor leagues. Initially Topps signed only players thought to have a high probability of making the major leagues until a scout declined to offer Maury Wills a contract while he was in the minor leagues. Wills won the 1962 National League Most Valuable Player award but refused to sign a contract with Topps until 1967 due to this perceived slight. Afterwards Topps signed virtually all minor league player to contracts. Miller (1991) states that Topps would sign minor league players for $5 plus $125 when they reached the major leagues. Fleer made minor headway by signing Ted Williams to an exclusive contract near the end of Williams’ career, but for the most part Fleer was relegated to producing cards of players no longer active in major league baseball. The FTC filed suit against Topps on February 8th, 1962, charging Topps with monopolizing the baseball card industry. Although the FTC action in 1962 failed, Fleer continued to pursue the possibility of producing baseball cards.8 According to Miller (1991), Fleer offered $25,000 plus 5% of receipts on 5×7 glossy photos, for which Topps did not have exclusive rights. The MLBPA declined and Fleer filed a lawsuit in June 1975 accusing Topps and the MLBPA of illegal restraint of trade. Fleer won this case against Topps although the MLBPA was cleared of wrongdoing,9 and was granted licenses by MLB and the MLBPA to produce baseball cards in 1981. At the same time, another company, the Donruss Company (Donruss), was also granted licenses to produce cards in 1981.

During this time period a typical set of cards produced by Topps would be released in multiple series over the course of the baseball season. Prior to 1957 the card size varied, but in 1957 Topps established what would become the standard or conventional card size of 2½” by 3½”. Topps would produce only one conventional brand each year, although Topps did produce some products that differed from the conventional brand either in size or in product type. For instance, in 1960 Topps produced a set of baseball player themed Tattoos, a set of “Giants” (cards larger than the conventional size) in 1964, and a set of stamps in 1969.10 Some items were printed for national distribution, while other items were tested in specific markets. This appears to be an early effort by Topps to develop a market for multiple baseball-related collectibles.

In addition, throughout the 1960s Topps would routinely insert “bonus items” into packs of cards, essentially a premium for its premium, as the stated primary purpose of the baseball cards was still to sell more gum. These bonus items were usually stamps, coins, transfers (tattoos), or posters of individual players or teams. These insert items are the precursors to the modern inserts, although most modern inserts are cards of the conventional size with a lower print run than the base set.

There is a slight increase in the number of inserts in the late 1960s and early 1970s. This increase may have come about due to the fact that the MLBPA was able to obtain an increase in the amount that Topps paid players for use of their likeness. Prior to 1969, each player received $125 for the year from Topps. After 1969, the player’s fee was increased to $250 and the MLBPA also received 8% of all revenues up to $4 million dollars and 10% on any amount over $4 million.11 Solomon (1973) reports that Topps sold 250 million cards in 1972.

8For a detailed discussion of this legal case, see Vernon (1992). 9See Fleer Corp. v. Topps Chewing Gum, 1980 10This list is by no means exhaustive. 11See Chapter 8 of Miller (1991).

2.2.1 Pricing Policies

From the years 1956-1973, cards were sold primarily through retail outlets in penny, nickel, or dime packs, which reflected the suggested retail price (SRP) for a pack of cards. The number of cards per pack was typically such that the price per card of a pack averaged a penny per card, although in the 1950s Topps’ nickel packs had six cards per pack, and the packs also contained one stick of gum. Topps would retain the policy of packaging cards at the rate of six cards for a SRP of five cents until 1961, when it began packaging the cards at a SRP rate of a penny per card. From 1961 to 1973, the SRP of a pack of cards would remain at a penny per card, although Topps would discontinue the use of penny packs and replace them with dime packs. Presumably Topps made this change to lower costs, as the number of packs that would need to be produced with this new system would be less than it was in the old system if the production numbers stayed the same, meaning Topps would have to purchase less wrappers to package the cards in and also produce less gum to insert into the packs. In 1974, Topps lowered the amount of cards per pack to eight while keeping the SRP of a pack at ten cents. This marks the first time that the ratio of SRP per pack to cards per pack exceeded one penny. From 1975-1977 Topps sold packs of 10 cards for 15 cents. In 1978 Topps would sell 14 cards for 20 cents, in 1979 12 cards for 20 cents, and in 1980 14 cards for 25 cents.

Topps also sold cards via cello and rack packs throughout this time. The term cello pack is derived from the cellophane wrapping that Topps used for these packs. Cello packs contained more cards than wax packs and the price/card ratio was slightly better for the consumer than in a standard wax pack. A rack pack is essentially three wax packs packaged together in one bundle. Although originally sold flat, the term rack pack likely originated when the packs were attached to a strip of plastic material with a hole in it so that they could hang on a rack at a retail outlet. Again, consumers typically received a slight discount when purchasing a rack pack when compared to three single packs.

2.2.2 Release Policy

During Topps’ monopoly years, it would typically release one brand of cards in a few series throughout the year. Some of these series of cards were printed in different quantities than the others (although in most cases the cards included in a series were printed at the same rate), with the latest series typically produced in the lowest amounts due to the time of its release near the end of the baseball season. Topps’ standard was to have 7 series, and this is true from 1959-1970. Prior to 1959 Topps was increasing the number of series each year, although this was likely due to the fact that the size of the base set was increasing each year (from 210 in 1955 to 572 in 1959). In 1974 Topps changed its release strategy. No longer were cards released in series, but all at once. From 1974 until 1992, Topps would release brands in this fashion, with two small exceptions in 1974 and 1976, when Topps issued its first traded sets.12 Topps’ rationale for this change from multiple series to a single series is visible on an advertisement on a Topps wax box in 1974, which explains that making all cards from the set available in a pack will “Keeps Topps baseball exciting and selling all season long”.

12A traded (or update) set features players who made a significant contribution during the season and were not included in the regular set of Topps or players who were traded during the season in their new uniforms. In 1974 and 1976, traded cards were only available in packs that could be purchased later in the year, while the regular cards were available in packs that could be purchased any time throughout the year.

2.3 Secondary market (1948-1980)

During the 1970s the increase in values of baseball cards was seen as a market explosion. Solomon (1973) reports that a Honus Wagner T206 card sold for $1,500 and that some cards from the 1950s sell for as much as $15 each while Gold (1974) reports that the Wagner actually sold for “only” $1,100. Addie (1975) reports that a 1952 Topps Mickey Mantle sells for $100 and that 1974 Topps San Diego/Washington variations are selling for $2 apiece, while Chapin (1974) reports that a 1952 Topps HI series of 96 cards had an offer of $1,600 but the seller refused, wanting $1,800. Putting this in perspective, in the 1940s legendary collector Jefferson Burdick created a price guide with suggested prices for cards. Burdick suggested vintage (tobacco cards prior to WWI) cards in good condition sell for 2 cents and more recent (gum and candy) cards should sell for 1 cent.

As prices of baseball cards increased the hobby became more noticed by the popular press. According to Chapin (1974), large conventions were held as early as 1969 in Southern California, and “The National” has been an annual event since 1971. There were dozens of publications dedicated to the hobby, but most were discussions of the hobby in general and not geared towards reporting prices. In 1979 Dr. James Beckett would publish The Sport Americana Baseball Card Price Guide. This book would become the standard for pricing throughout the hobby, and would ultimately lead to the creation of the monthly magazines published by Beckett publishing. As there is during every time period, collectors had two major complaints: rising prices and too much product. Little did they know what was to come.

3 Between Strikes (1981-1994)

In 1981 the Donruss Company (Donruss) and Fleer began production of baseball cards featuring active players, marking the first time in 25 years that more than one manufacturer produced a significant set of cards of active players. In 1981 Donruss and Fleer included a piece of bubblegum in their packs, but an appeals court ruled that Topps did have the monopoly right to the production of baseball cards with confectionery products as well as the monopoly right to sell baseball cards without tying them to another product.13 After the appellate ruling, Fleer packaged its baseball cards with stickers while Donruss packaged its cards with puzzle pieces. If baseball cards were previously viewed as promotional tools to sell bubblegum this decision by Donruss and Fleer to continue production without tying the cards to a confectionery product marks the beginning of baseball cards as a stand alone product.

The three manufacturers produced card sets from 1981-1987 with little competition. There only other manufacturer granted a license by MLB and the MLBPA was Optigraphics, Inc., which produced the Sportflics brand of baseball cards. Sportflics was introduced in 1986, and were actually quite different from traditional baseball cards. Sportflics cards had three pictures that appeared on the card front depending on how the card was tilted when held. Some of the cards, if moved quickly enough, showed a player “in action”, either swinging the bat, pitching, or fielding a ball. Since they were so different from the traditional cards, Sportflics were viewed more as a novelty than conventional brand, and their inclusion as a competitor to Topps, Fleer, and Donruss is borderline. In the Owner’s Box column in the February 1989 issue of Beckett Baseball Card Monthly (BBCM) the decision to exclude Sportflics from monthly pricing is announced, citing lack of collector interest in the product. In 1988 Optigraphics produced a conventional set, Score, in addition to Sportflics. In 1989 MLB and the MLBPA granted licenses to a fifth manufacturer, the Upper Deck Company (Upper Deck). Upper Deck was the first company created solely to produce sports cards. From 1989 until 1995, the baseball card industry would consist of these five manufacturers — Topps, Fleer, Donruss, Score,14 and Upper Deck. An additional license was granted to Pacific Trading Cards, Inc. (Pacific) in 1993, but it was not a full license. Pacific could only produce cards that were bilingual (English/Spanish) in nature, and Pacific released at most two brands a year from 1993 to 1997. These are not the only companies that have applied for licenses. Companies such as Classic, Frontline, and Action Packed applied and were denied licenses to produce picture cards distributed in pack form on a national basis. Classic was granted a license to produce picture cards as part of a board/trivia game in 1987, and continued production in this format until 1993 when it switched to producing minor league baseball cards.

Upper Deck’s entry into the market ushered in a new era for baseball cards as Upper Deck packs and cards differed from the traditional brands in three important ways. First, Upper Deck packs were foil packs rather than the traditional wax pack. A problem throughout the hobby was that wax packs could be opened, the valuable cards removed and replaced with less valuable cards, and then resealed to look like they had not been opened. Upper Deck’s foil packs needed to be torn to be open, and repairing them in a manner to be consistent with the pack being unopened was extremely difficult, if not impossible.15 Second, Upper Deck included a tamper proof hologram on its cards. Another problem in the hobby was that along with rising secondary market prices came counterfeit cards. The hologram made it extremely costly to counterfeit the cards. Finally, the quality of the Upper Deck cards was much higher than the quality of the other brands. Previously, high quality cards were released on a limited basis and were only available in factory set form (80s Topps Tiffany and Fleer Glossy cards), although Topps’ Sy Berger states that, “Our (Topps’) people had done all the research and we had the capability to make an upscale product back in the ’70s. We just didn’t know how our longtime collectors would react”.16 Upper Deck had a noticeable impact in the appearance of other manufacturers’ cards. Comparing Topps cards from 1952 to cards from 1990, little difference is seen in the quality of the card beyond the advances in basic photography and printing. In the later years, the photos were crisper and the cards were cut more evenly, but the overall quality of the cards did not change dramatically. Following the introduction of Upper Deck, cards became glossier and were printed on higher quality card stock. In effect, the popularity of Upper Deck’s initial release forced the other manufacturers to upgrade the quality of their cards. This would ultimately lead to manufacturers creating multiple product lines of differing quality, catering to different market segments.

Many innovations of the early 1990s have become staples in products currently released. In 1990 Upper Deck had Reggie Jackson autograph and hand serial number 2,500 copies of a particular card. These cards were then inserted into Upper Deck HI series packs. While Fleer had been providing inserts in its packs since 1986, the serial-numbered certified autograph card of Reggie Jackson was a major change in the type of insert card available. In 1991 Donruss became the first manufacturer to provide serial numbers for a set of insert cards, its Elite series. Rather than hand-numbering, these cards were stamped with an individual serial number (e.g. 00432/10000). In addition to providing the production run of the cards, this also serves as some protection against counterfeiting. In 1992 Topps and Donruss both introduced parallel cards, Donruss with its Leaf Black Gold and Topps with its Topps Gold. A typical parallel card will have the same photograph as the card from the base set but the insertion rate for parallel cards is typically lower and there is usually some distinctive change in the border of the card that allows collectors to determine it is a parallel. For instance, the borders of the basic set of 1992 Leaf are gray while the borders of Leaf Black Gold are black while Topps used gold foil for the lettering in its Topps Gold set. Both manufacturers inserted their parallel cards at a rate of 1 per pack in 1992. In 1993 Topps introduced refractors in its Finest product. Refractors are parallel cards that use a special coating that refracts light. In addition, the refractors were in extremely limited supply for that time period with a stated print run of 241. In 1993, Pinnacle Brands Inc. (formerly Optigraphics) would release the production numbers for two products, Select and Select Rookie/Traded, by serial-numbering the cases of the products. This decision to serial number the cases of these products was made in response to a gaffe in 1990 when 1990 Score was believed to be in short supply early in the year. The price for the complete set of 1990 Score cards increased rapidly based on this perceived short supply. However, late in the year a large number of unopened cases of 1990 Score appeared on the market after additional product was shipped. The complete set price dropped quickly, and collector confidence in Score products was shaken. This loss of collector confidence would eventually lead to Optigraphics renaming itself Pinnacle. In 1994 Fleer introduced die-cut cards to the baseball card market. These cards are the same “size” as a standard baseball card, but the cards are die-cut to enhance the look of the card. The earliest cards were Fleer’s Hot Gloves in 1994 Flair, in which each card was die-cut to look like a baseball glove.

13See Topps Chewing Gum v. Fleer Corporation, 1982 14Score would change its name to Pinnacle Brands, Inc. in 1992. 15Score had attempted to solve this problem in 1988 by packaging its cards in what was essentially a plastic bag that needed to be torn to be open. However, packs were still “searchable” given that Score used a see-through bag. 16This is in the Topps Factory Tour, April 1996, pg. 24, by Portantiere.

3.1 Release Policy

When Fleer and Donruss first produced cards in 1981, they followed the same release strategy as Topps. Both companies had one brand and one release, in which all the cards for the brand were available in the packs of that release. Other than the production of Fleer and Donruss cards, the major hobby news that occurred in 1981 was that Topps brought back the traded set concept that originally debuted in 1974. However, Topps released the traded cards through hobby stores in factory set form in 1981, not in packs. This marks the first time in which a manufacturer released a major product without releasing it in retail outlets. Throughout the 1980s the manufacturers followed a fairly standard release schedule — all of them would release their primary products between November and February. For example, 1989 Score was available in late November of 1988. Near the completion of the baseball season, around the middle of October, the manufacturers would release their traded or update products, always in factory set form. Between the release of their primary product in November—February and the release of their traded set the following October, companies would release products for other major sports and entertainment as well as other baseball products. These other baseball products have been given the name “oddball” products by collectors. These products differ from the regular issues in a number of ways. The actual physical size of the card may be different (either larger or smaller), the number of cards in the set is smaller, the quantity of cards produced is typically lower than that of the primary products, and the sets contain only star players or rookies. Oddball products also consist of products that are not cards, such as stickers, coins, and tattoos, that were produced in an attempt to reach a wider audience. All three manufacturers released oddball products in pack form as well as in factory set form throughout the 1980s, and the production of oddball products may be viewed as another attempt at producing multiple brands by the manufacturers, similar to Topps’ oddball releases in the 1960s.

In 1989 Upper Deck would release its product in two series. However, this release was unlike when Topps released cards in series during its monopoly years. First, Upper Deck released a standard size set of 700 cards in its first series. Its second series was essentially its traded set, and it contained only 100 cards, most of them rookies or updated versions of players who switched teams after Upper Deck released its first series. In addition, Upper Deck’s second series was available in packs along with the cards from the first series. The release of a product in series would prove to have an advantage. Given that Topps signs players to individual contracts Topps can include any player under contract in its sets.17 Since the other manufacturers only sign a licensing agreement with the MLBPA they can only include players currently on a team’s 40-man roster. Thus, Topps can include cards of players before they reach the major leagues, giving Topps an advantage in the rookie card market. The release of a product in series allows time for some young players to be added to the 40-man roster during the season, and allows the other manufacturers to produce rookie cards of some of these players.

In 1989, Topps became the first manufacturer to release two different major brands18 in pack form on a nationwide basis when it brought back the Bowman brand of baseball cards. Bowman’s consideration as a major set lagged its release date as Bowman was released in June but would not be priced in BBCM until September. This decision is mentioned in the Owner’s Box column of the September 1989 BBCM. This introduction of a second major brand, coupled with the change in quality brought about by the entrance of Upper Deck, would change manufacturers’ release strategies during the 1990s. The manufacturers began by releasing a second product which would compete with the Upper Deck flagship brand. The second product was typically higher quality with a lower print run than the flagship brand. Donruss would launch Leaf in 1990, Fleer would release Ultra in 1991, Topps would release Stadium Club in 1991, and Pinnacle would release Pinnacle in 1992. Upper Deck would actually release a less expensive product in 1994, called Collector’s Choice, to compete with the lower priced brands.

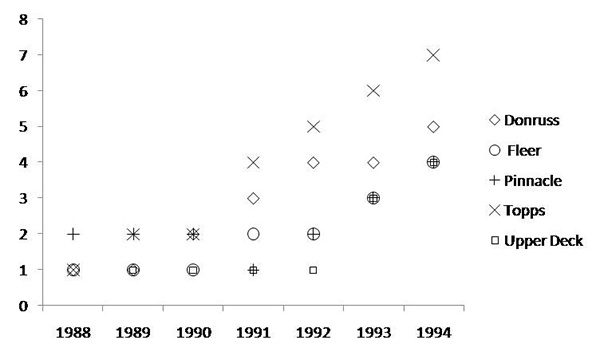

Figure 1: Number of brands by manufacturer from 1988-1994.

By the 1994 most manufacturers had at least 3 different established brands, with the brands aimed at different segments of the market. Figure 1 shows the total number of brands by manufacturer from 1989-1994. Donruss had Donruss (1981), Leaf (1990), and Studio (1991). Fleer had Flair (1993), Fleer (1981), and Ultra (1991). Pinnacle had Pinnacle (1992), Score (1988), and Select (1993). Topps had Bowman (1989), Finest (1993), Stadium Club (1991), and Topps (1951). And Upper Deck had Collector’s Choice (1994), SP (1993), and Upper Deck (1989). Collectors would refer to the brand quality levels as basic, premium, and super-premium.

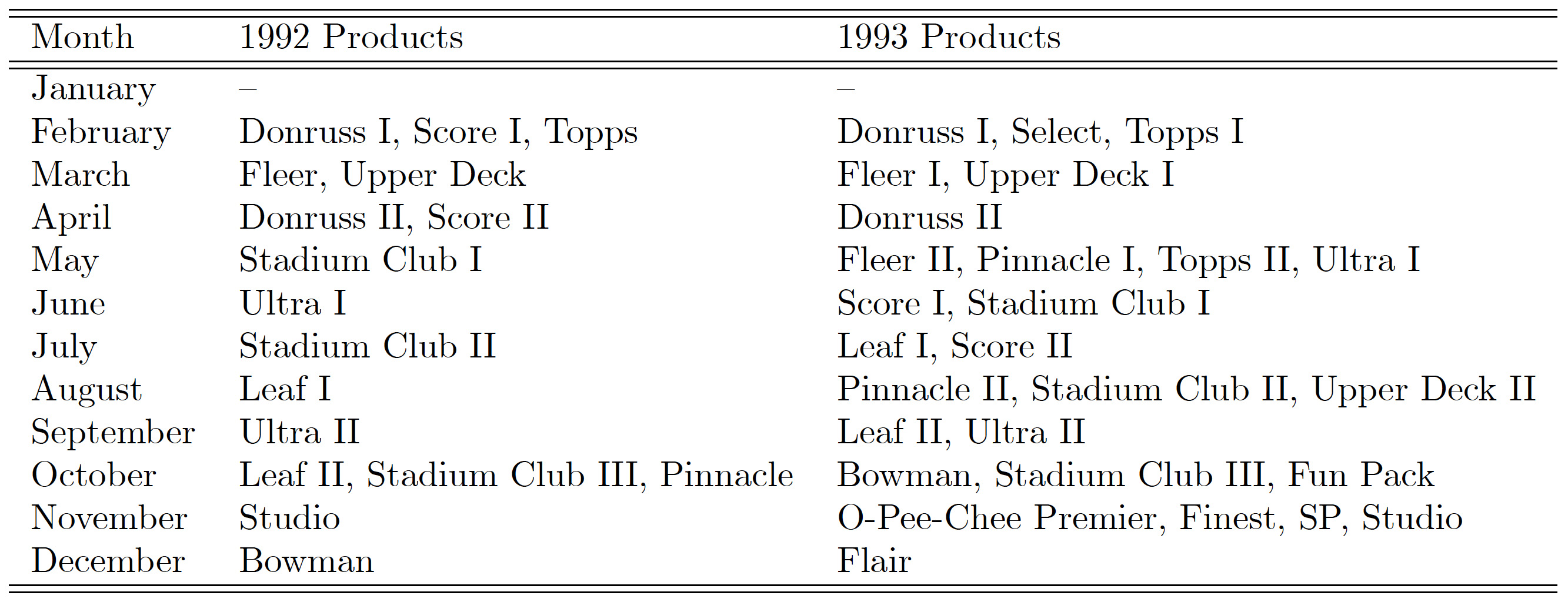

As multiple brands were being released, the standard release pattern for manufacturers would be for manufacturers to continue releasing their flagship products after the baseball season but before Christmas and then to release their premium and super-premium products during the baseball season. One reason may have been to stimulate interest in the new product lines, as the established product lines had a more established collector base, and products released in the summer would be released during the baseball season. Bowman, which would begin to focus on rookie cards of players in the lower minor league levels, was produced near the end of the year to allow more time for these potential prospects to mature. While the exact release dates for products from this era is not available, approximate release dates can be determined using the first appearance of a product in the monthly price guides. Table 1 lists the appearance in BBCM of each product by month for 1992 and 1993.

Table 1 also shows that in addition to the creation of more brands there were more product releases as manufacturers returned to releasing products in series. One benefit to releasing products in series is that a previously unknown or lightly regarded player could have a breakout year, and the manufacturers could include this player in a later series. In essence, this was Upper Deck’s strategy in 1989 when it released its high series, which included rookie cards of players who would not have been available earlier in the year. Also, if a particular product does not sell well, then production plans for its later series can be changed or scrapped altogether.19 Alternatively, if a particular product does well but is not scheduled for multiple series releasing additional series can be used to extend any excess profits that result from a brand surpassing expectations. One brand released in 2002, Topps 206, was a new brand from Topps. It quickly rose to the top of most consumers’ want lists, and Topps released two follow-up series that were not scheduled for release in order to capture any excess profits resulting from the brand being so well received by consumers.

Table 1: The month of first available pricing for 1992 and 1993 products.

17This process changed in 2006 as MLB and the MLBPA began limiting which minor league players could appear in major league sets. 18Optigraphics, the company that would become Pinnacle, had released Score and Sportflics in both 1988 and 1989, but as has already been mentioned the inclusion of Sportflics as a competitor to the other brands is borderline at best. The Sportflics brand is viewed by many to be similar to the oddball products previously mentioned. 19It appears that this happened with 1995 Topps DIII as only the first series was produced.

3.2 Pricing Policies

In 1981, Topps released its product with a suggested retail price (SRP) of thirty cents per pack of 15 cards. Fleer and Donruss also had SRPs of 30 cents per pack in 1981 but Fleer’s packs included 17 cards while Donruss’ packs included 15. From 1982 to 1984, all three manufacturers had fifteen cards per pack with a SRP of 30 cents. In 1985 the SRP of packs began to rise, usually by 5 cents every one or two years, with Topps reaching 55 cents in 1992. Cards per pack for the flagship brands remained between 14-16 cards during this time. In 1993 Topps’ packs included 15 cards for 69 cents and in 1994 14 cards for 79 cents. The only manufacturer which did not follow this pricing policy for its flagship brand was Upper Deck, which had an SRP of $1 for 15 card packs of its Upper Deck brand.

For premium and super premium brands the pricing was quite different. Unlike their flagship products, premium and super premium brands of this era rarely carried SRPs stamped directly on the packs or on the boxes of the product. This is likely to allow retailers to be able to adjust prices based on market conditions. As an example, 1991 Stadium Club carried a SRP of $1.25 per pack. However, the Reader’s Write of BBCM during 1991-1992 is littered with objections about having to pay $5 or more per pack. Similarly, although no SRP is cited, it is unlikely that Topps released its 1993 Finest product with a SRP of $25 per pack, but complaints (always by buyers) are rampant throughout the hobby periodicals during 1993-1994 about the exorbitant cost of the product. This lack of a clearly provided SRP by the manufacturer would carry over into later years when manufacturers began releasing the “same” product through hobby and retail channels, although the hobby product typically had better odds of pulling a rare card. The retail package would typically contain a SRP while the hobby package would not.

3.3 Secondary Market

The secondary market in the 1980s and early 1990s was defined by individuals stockpiling cards, particularly rookie cards, of players and swapping them like shares of stock, and by collectors attempting to discover variations and errors in their cards in the hopes of finding a rarity. At the tail end of this time period demand for parallel and insert cards began to spike. Advertisements for lots of 25, 50, 100, and even 500 of the SAME card were prevalent throughout this time period.20 Rookie cards, which provided the most speculative potential given that the player pictured on the card had little to no major league experience, were in particularly high demand. Many magazines touted the fact that a 3-cent Dwight Gooden rookie in 1985 had reached $2 by the end of the year, although provided little mention about those rookies who did not pan out. Sing (1988) points out that baseball cards were one of the hottest investments in 1988, citing the increase in price of the 1952 Topps Mickey Mantle card. Hershey (1989) specifically mentions baseball cards, along with art, as a means of diversifying one’s investment portfolio. Prior to limited insert sets, finding an error or variation was the method of obtaining a card that was relatively more scarce than the others. The search for errors and variations would become so popular that Beckett would begin a column called Errors and Varieties in the June 1988 issue of Beckett Baseball Card Monthly. Finally, along with high secondary market prices came individuals who produced counterfeit cards in an attempt to profit off of uninformed collectors. These concepts are discussed in detail.

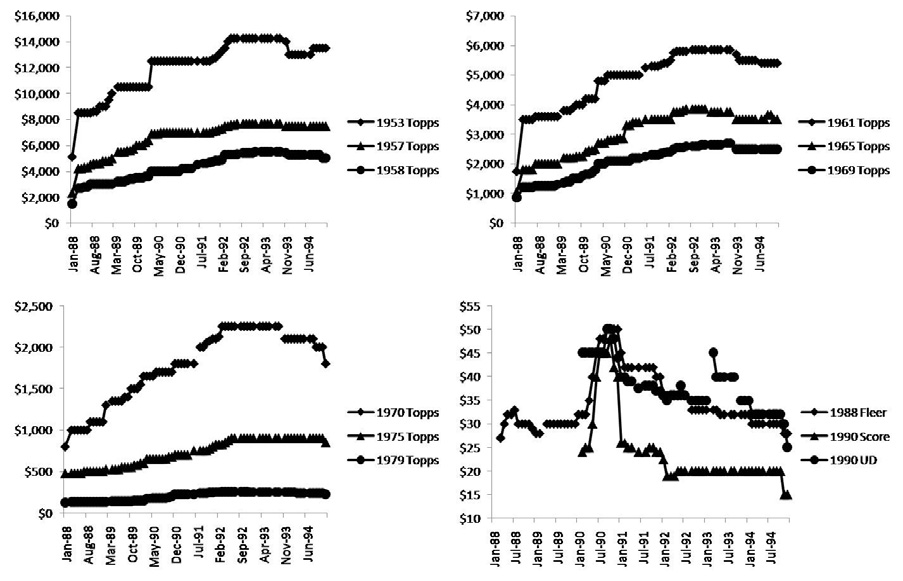

Figure 2: Secondary market prices for selected sets from the 1950s-1990s.

Figure 2 shows complete set prices from April 1988 until December 1994 for selected brands. The top left panel shows the price path for complete sets of 1953, 1957, and 1958 Topps cards, the top right panel the price path for the 1961, 1965, and 1969 Topps sets, the bottom left panel the price path for the 1970, 1975, and 1979 Topps sets and the bottom right panel the price path for the 1988 Fleer, 1990 Score, and 1990 Upper Deck sets. These price paths are typical for sets of this era. Complete set prices are used rather than individual card prices because complete set prices are typically less volatile than individual cards. While complete set prices due tend to fluctuate as the key rookie cards in the set fluctuate, most of the sets from the 1950s and 1960s featured rookie cards of players who were inactive by 1988 and thus the values of those sets were not affected by on-field performance of the players.21 As the panels for the 1950s, 1960s, and 1970s sets show, there were virtually no declines in the post-WWII material until late in 1993 — over 5 years of growth.22 However, the more recent brands show sharper declines than the older brands and the decline occurs earlier in most cases. Part of the change is due to fluctuations in value of key rookie cards during this time period, but the general decline in set values for newer products reflects how the industry had changed in response to the introduction of insert cards.

20This is described in Thomas (1988) and can also be seen in advertisements in baseball price guides such as Sports Collectors Digest. 21The notable exceptions are the 1968 and 1969 Topps sets which include the rookie card and second-year card of Nolan Ryan, who was the only superstar player still active in 1988 from these sets. 22There are some changes in the listed card grades during this time. From Jan. 1993 to Feb. 95 cards from 1968-1979 are listed in NM-MT condition. In Feb. 95 BBCM changed its listed grades to NrMT for the 1968-1973 products and while leaving the 1974-1979 products at NM-MT.

3.3.1 Rookie Cards

With the increase in visibility, speculators entered the market and in the 1980s stockpiling of cards, particularly rookie cards, became a major craze. Although the definition of a rookie card has changed over time, it is generally defined by the hobby as the first nationally distributed card of a player in a brand of cards, as long as that player has not had a card in a brand of cards from the manufacturer of that brand or another manufacturer in an earlier year. Rookie cards are a staple in the hobby, and their appeal to collectors has driven some recent changes in when manufacturers release products.

The rookie card concept is best explained by example. In 1983, Topps, Donruss, and Fleer all contained their first cards of Tony Gwynn, so all three cards are considered rookie cards. In 1984, Fleer and Donruss both contained a card of Kevin McReynolds, so they were considered his rookie cards. Topps, however, did not have McReynolds under license then, and would not release its first card of McReynolds until 1988. The 1988 card has never been considered a rookie card, although it is considered his First Topps Card, a label which had more importance in 1988 than it does today. Moving forward a few years to when manufacturers were releasing more than one brand of cards in a year, consider the case of Derek Jeter. In 1993, Jeter had cards in 8 brands (Bowman, Pinnacle, Score, Select, SP, Stadium Club Murphy, Topps, and Upper Deck) from 3 manufacturers (Pinnacle, Topps, and Upper Deck). All 8 cards are considered rookie cards by the hobby. However, neither Fleer nor Donruss produced a card of Jeter in 1993. When Fleer and Donruss eventually produced their first cards of Jeter in 1995 and 1996 respectively, neither card has ever been considered a rookie card.

Historically, rookie cards have been the most valuable cards because they were the oldest and usually the most scarce cards of a player. There are exceptions to this however — Mickey Mantle’s true rookie card is his 1951 Bowman card, but his 1952 Topps card is his most valuable card due to the fact that it is the first Topps card of Mantle and that the card was included in the scarce high series of 1952 Topps. Recently, given that rookie cards exist in multiple products and that certain insert cards are more scarce than rookie cards, the focus has shifted to obtaining the player’s best card, which likely contains a manufacturer certified autograph. However, rookie cards still generally carry a premium over most later released base set issues.

3.3.2 Error Cards

In addition to rookie cards, error cards also played a prominent role in the 1980s market. The term error card refers to any card that has any type of mistake — photo of an incorrect player, incorrect biographical data for the player, incorrect team, incorrect statistics, misspelled words in text on the card back, and printing defects are just some of the potential error cards. In the 1930s and 1940s, when baseball card collectors had no checklists and were still cataloging which cards existed, finding a variation was like finding a new card. Thus, the Sherry Magee error card from the 1909 T206 set,23 in which his last name was spelled Magie, was valued more than others, even as far back as the 1940s, because it was rarer.24 This portion of the hobby carried over into the 1980s with collectors looking for anything that could make their particular card rarer and hence more valuable. In one of the few academic articles on the manufacture of baseball cards, Stoller (1984) ponders how an industry built on scarcity and quality of the cards will exist and predicts that error cards will become the norm in the industry. For a certain period of time it looks like he is correct as in the 1980s finding and cataloging errors became an obsession within the hobby. The Readers’ Write, a forum in which collectors could ask questions about baseball cards, was littered with questions about finding potential error cards and their value. There was an Eagle Eye award for a collector who spotted the “toughest” error.

Error cards only have value above typical market value if they are corrected, resulting in the error cards being relatively more scarce than other cards produced. In the 1960s most error cards consisted of misspelled names, photo changes, and printing variations, and relatively few were corrected. The most valuable error cards are the 1969 Topps “white letter” variations for some players where the letters of the players’ last names are printed in white rather than yellow. In the 1970s there were also relatively few error cards — the most valuable are the 1974 Topps “Washington, Natl. Lg.” cards. There was a rumor that the San Diego Padres would move to Washington D.C. in 1974, and Topps printed cards of Padre players with “Washington” for the team location and “Nat’l. Lg.” for the team name. The Padres did not move, and Topps corrected the cards in later print runs. However, from 1975 to 1981 Topps would only correct one error, the 1979 Topps Bump Wills card that incorrectly listed his team as the Blue Jays on the front of the card. In 1982 there were only 3 corrected errors, and from 1983-1986 there are no corrected errors in Topps’ cards. In 1987 there are a few cards with printing defects, either missing copyright dates or trademark (TM) logos. It was curious that 2 of the 3 cards missing the trademark logos were of two of the hottest players in the market, Don Mattingly and Dwight Gooden. This led to accusations that Topps deliberately left the TM logo off of these two cards to create interest in the product. However, in 1988 and 1989 there were few corrected errors and most of those involved printing flaws. In 1990 Topps had one major error that was corrected, the Frank Thomas card that was printed without his name on the front. The 1991 Topps set contained its most errors ever, with many errors containing incorrect biographical information which would subsequently be corrected. From 1992 until the present Topps would produce some cards with uncorrected errors, but would correct few of them.

The other manufacturers had similar patterns for error cards. In 1981 Donruss and Fleer had multiple printings of their cards, using the latter printing to correct errors made in the initial print funs. These errors were likely not deliberate but due to time constraints in bringing their products to market after being granted licenses by the MLB and MLBPA. This claim appears to be substantiated by the fact that Fleer had few errors in its 1982 product, one printing error in its 1983 product, and then no corrected errors from 1984-1987. Donruss had minor issues with misspelled names and printing variations in 1982 and 1983, no corrected errors in its 1984 product,25 and relatively few corrected errors in its product from 1985-1989. In 1990 Donruss had some cards with reverse negatives, and its entire All-Star subset had the text “Recent Major League Performance” instead of “All-Star Game Performance” printed above the statistics on the card backs. In 1991 there were a few corrected errors and from 1992 and beyond there were no corrected errors. As for Fleer, in 1988 their product would contain multiple cards with misspelled names and incorrect photos of players that would subsequently be corrected. In 1989 Fleer produced the most infamous “error” card, known in the hobby as the “Rick Face” card due to its designation by BBCM. The “Rick Face” card features Billy Ripken with an easily discernible obscenity visible (i.e. no magnifying glass is needed) on the knob of the bat in the photo. Fleer used multiple methods to remove the obscenity in future printings, and the attention given to this “error” may have spurred other manufacturers to make errors. In addition to the Rick Face card there were multiple cards originally printed in Fleer’s 1989 product with incorrect biographical information that were subsequently corrected. From 1990-1992 Fleer had only a handful of corrected errors each year and after 1992 there were no corrected errors.

The two newest members to the industry, Score and Upper Deck, had some corrected errors in their initial products. In 1988 Score misspelled a half dozen names on the fronts of the cards and in 1989 and 1990 there were a few misspellings and incorrect uniform numbers assigned to players. In 1991 and 1992 Score’s flagship brand still contained many uncorrected errors but none were corrected and by 1993 even the uncorrected errors had been reduced to a single one. In 1989 and 1990 Upper Deck’s initial production runs contained various errors (incorrectly identified players, reversed negatives, etc.) but by 1991 Upper Deck reduced the number of corrected errors to 2 and from 1992 and beyond it was rare to see a corrected error.26 The only notable corrected error occurred in 2002 Upper Deck Vintage and was a printing flaw where the names of the players on the homerun leader card were missing. Pacific, the last manufacturer to enter in this time period, had 2 corrected errors in its initial product in 1993 and none thereafter.

By 1993 there were relatively few corrected errors. The cause of this reduction can likely be linked to several factors. First, with improvements in printing technology the variations which existed due to printing flaws was reduced. Second, error cards were primarily valued on the secondary market for their scarcity, but manufacturers had begun to create numerous insert sets that were even more scarce than the base set, reducing the need for errors to fill this scarcity void in the hobby. Finally, since the manufacturers were now producing multiple products it is likely that creating a separate printing simply to correct a few mistakes was not as profitable as creating a new product. The error craze would come to an end, but Upper Deck would commemorate it by releasing a parallel set in its 2002 UD Authentics product called “reverse negative”, in which the parallel cards were all printed with reverse negatives.

23This is the name given to the set by Jefferson Burdick in The American Card Catalog. The set was produced by the American Tobacco Company. 24Cady (1973) reports that the Magie error card is selling for $100. 25In 1984 each of the first 26 cards in Donruss has a variation and there are 2 cards that have versions with and without card numbers. However, these variations are due to separate printing for its packs and factory sets. 26Williams (Card Sharks) states that some individuals at Upper Deck believe that Upper Deck deliberately created these errors.

3.3.3 Insert cards

Insert premiums had been around since the 1950s, but mainstream interest in them did not occur until the early 1990s. The Fleer All-Star set in 1986 is recognized as the first modern insert set, and for some time these insert cards were priced in the monthly Beckett guide. However, in May 1989 the cards were removed from BBCM’s price guide. Donruss would include Bonus MVPs as inserts in some of its later print runs from 1988-1990, but these cards are essentially as available as base cards from those brands. The 1990 Upper Deck Reggie Jackson autograph and 1991 Donruss Elite series sparked interest in inserts, and the initial parallel sets by Topps and Donruss also generated interest in insert sets. The Elite series, serial numbered to 10,000, sparked such immense interest that stories exist that individuals searched cases of the 1991 Donruss product with metal detectors in an attempt to detect the foil serial numbering. The insert set that would sustain the most interest would be the 1993 Finest Refractors (produced by Topps), with a stated print run of just 241. At a time when the vintage market was leveling off and interest in newer product base sets was waning the Finest Refractors showed extraordinary growth. Further discussion on the pricing of insert sets will be discussed in section 4, but as late as 1996 the Finest Refractors were still among the hottest cards on the market.

3.3.4 Counterfeits

With the increase in secondary market values came counterfeiting attempts. Given the hobby’s interest in rookie cards, most counterfeited cards were of the priciest rookie cards. It is well-known within the hobby that the 1952 Topps Mickey Mantle, the 1963 Topps Pete Rose, the 1982 Topps Cal Ripken, the 1984 Donruss Don Mattingly, the 1984 Fleer Extended Roger Clemens and Dwight Gooden, the 1986 Donruss Jose Canseco, and the 1990 Leaf Frank Thomas cards were all popular targets for counterfeiters. Various issues of BBCM specifically mention these cards as potential targets for counterfeiters. Some innovations by the industry were designed to thwart counterfeiters. One was Upper Deck’s inclusion of a hologram on the back of the card, making it difficult to reproduce. Another was the serial-numbering of cards — if a collector ever saw two cards with identical serial numbers he could be assured one of them was counterfeit. Also, the steady increase in quality of the cards in addition to the technological advances and inclusion of game-used memorabilia and autographs made it much more difficult for counterfeiters.

In the early 1990s card grading services emerged. While card grading services primarily focus on grading the card based upon its appearance, the more prominent services also check for counterfeits or cards that have been altered (retouched or trimmed) in an attempt to make the card appear higher quality. While there are numerous grading companies, three companies products carry a premium on the secondary market — Professional Sports Authenticators (PSA), Sportscard Guaranty Corporation (SGC), and Beckett Grading Services (BGS). A fourth company, Global Authentication, Inc. (GAI) also carries a premium, although recent events may downgrade collector confidence in GAI.

4 Product Proliferation and Industry Consolidation (1995-present)

After the player’s strike in 1994, the sale of baseball cards slowed considerably, in part because the players’ strike alienated the casual baseball fan. According to Ambrosius (2002), new card sales for the sportscard industry peaked in 1991 at $1.2 billion and declined every year through 2001 when new card sales were at $350 million. Davies (2007) reports that sales in 2005 were around $250 million and had increased to $270 million in 2006. This general decline in the past 15 years has led to a shifting industry landscape. The first change in the industry was the acquisition of Donruss by Pinnacle in April of 1996, which reduced the number of fully-licensed manufacturers from five to four. The next change occurred in May of 1998, when Pacific was granted a full license to produce cards, returning the number of fully-licensed manufacturers to five. However, Pinnacle would file for bankruptcy in July of 1998, reducing the number of manufacturers to four, and the brand names of Donruss and Leaf would be acquired by a non-licensed company, Playoff, Inc. (Playoff). Although Playoff was allowed to release one product that Pinnacle had already manufactured in 1998 (Leaf Rookies & Stars), it was not granted a license by MLB and the MLBPA until February 2001. However, the number of fully-licensed manufacturers did not return to five in 2001 as Pacific decided not to renew its license to produce baseball cards. In 2006 Playoff was declined a license, and Fleer filed for bankruptcy and was subsequently purchased by Upper Deck, leaving the baseball card industry with less than 3 manufacturers for the first time since 1980. The article began with a discussion of Upper Deck’s attempt to purchase Topps, which if successful would send the industry back to a monopoly.

The dominant trend throughout most of this period would be the increased number of brands released each year by all manufacturers. In the previous section it was discussed how these different products were aimed at different segments of the market based on perceived quality of the cards (regular, premium, superpremium). In the late 1990s and early 2000s, manufacturers produced sets aimed at even narrower target audiences. For example, Topps was producing three lines of Bowman cards (Bowman, Bowman Chrome, and Bowman’s Best) all targeting rookie card collectors at three different quality levels. Some sets, such as Topps’ Topps Laser and Superchrome, Pinnacle’s UC3, and Pacific’s Crown Royale, were produced to showcase a particular technology in a standard set as opposed to only using the technology in insert sets. In fact, the technology had changed so much that Pinnacle released its own technology glossary. Other sets focused on specific teams (Upper Deck’s Yankees Legends and Fleer’s Red Sox 100th Anniversary) or very specific themes (Upper Deck’s Challengers for 70, which included those players likely to challenge the then single season record of 70 homeruns). These sets were in addition to the manufacturers’ already established flagship, premium, and super-premium sets. A further discussion of the release policy will follow.

Another trend was the dwindling production run of insert and parallel cards. Given the frenzy created by the Topps Finest Refractors insert set in 1993, which had a stated print run of 241, a further decrease in print run for some insert sets is a natural extension. Perhaps due to the MLBPA strike in 1994 and declining interest in baseball related products in general, most insert sets in 1994 and 1995 remained at fairly reasonable stated production levels around 1000 or 2000. There are some exceptions, but these were primarily parallel sets with unannounced print runs, such as Topps’ Stadium Club First Day Issue (available 1:36 packs), Upper Deck’s Collector’s Choice Gold Signature (1:36 packs), and Pinnacle’s Pinnacle Artist’s Proofs (available 1:26 packs) and Sportflics Rookie/Traded Artist’s Proofs series (1:24 packs). In 1996 Pinnacle released Select Certified, which contained 6 different parallel sets. The most easily obtainable parallel cards in this set were the Certified Red, available at a rate of 1:5 packs. However, the Mirror Blue and Mirror Gold parallel cards had stated print runs of 45 and 30 respectively, with insertion rates of 1:200 and 1:300 packs. In 1997 the boundary was pushed to its limit when Fleer and Pinnacle would produce one-of-one inserts. Pinnacle’s first one-of-one insert was a redemption card for a 24K solid gold coin of the specified player in its Pinnacle Mint brand. These redemption cards were inserted approximately 1:47,200 packs. Pinnacle would also cut up the printing press plates for its 1997 New Pinnacle brand and insert these plates in packs. The four color printing process requires a total of 8 plates, one of each color for both the front and the back of the card. Since the plates are different colors each is essentially a one-of-one item. The first true one-of-one cards produced were by Fleer for its Flair Showcase product. These cards, dubbed Flair Showcase Legacy Masterpiece, were viewed with mixed reactions.27 The one-of-one parallels and other extremely low numbered cards would not become a product staple until Playoff began producing cards in 2001.

One innovation that caught new life in this period was the buyback card. A buyback card is a card that was produced by the manufacturer at an earlier date, then bought on the secondary market by the manufacturer and randomly inserted into the manufacturer’s current product. Topps had used buybacks in 1991 for its 40th anniversary, inserting either actual cards or redemption cards for the original cards.28 In 1996, Topps repurchased original Mickey Mantle cards and then packaged redemption cards for a lottery of the original Mantle cards. In 1997, Upper Deck would repurchase cards from its 1993-1996 SP brands and have the pictured player autograph the repurchased cards. The autographed cards were then hand-serial numbered and randomly inserted into packs of 1997 SP Authentic. Each card also came with a certification sticker on the back of the card and a certification card with a number that matched the sticker. The serial-numbered and autographed buyback card would become a staple of future products, particularly those focused on retired players.

The use of redemption cards by manufacturers also became more prominent. If a consumer receives one of these redemption cards, he can redeem it for the item specified on the redemption card. In the past redemption cards were used primarily for items that were too large to fit into a pack of cards, perhaps an additional set of cards, a particular player’s game-used bat, or a chance to win a trip to a World Series game. Currently, redemption cards are also being inserted for objects such as autographed cards and rookie or 1st year cards, both of which fit in the card pack. The stated reason for issuing redemption cards for autographs is that the player autographing the card did not return the autographed cards to the manufacturer in time for the manufacturer to include them in the packs when the product was scheduled to ship. As for the rookie card redemptions, these are typically redemption cards for unknown rookies that may emerge during the upcoming season, and these types of redemptions are inserted in brands released early in the baseball season (about January to July). The reason for the inclusion of these redemption cards is to ensure that the brands released early in the season do not miss any of the key rookie players who may have an impact during the year. In either case, manufacturers could avoid inserting redemption cards by delaying the release of the brand, which occurs in rare cases.

In 1996 Donruss would push the insert set to a new level with its Leaf Signature product. Packs of Leaf Signature carried a then unheard of SRP of $9.99 for 4 cards but each pack included at least one certified autograph card. The change with the largest impact would occur in 1997 when Upper Deck introduced the game-used memorabilia card to the baseball card hobby.29 A game-used memorabilia card is a standard sized baseball card with a piece of the depicted player’s memorabilia embedded into the card. The initial cards were inserted every 800 packs in 1997 Upper Deck Series I and featured game-used jerseys of Ken Griffey, Jr., Tony Gwynn, and Rey Ordonez. Ultimately, game-used cards would include bats, hats, shoes, gloves, helmets, baseballs, and bases. Upper Deck would use a similar process to create cut signature cards, which are embedded autographs of deceased players into cards. By acquiring cancelled checks or authenticated autographs of deceased players Upper Deck was able to remove the autograph from the original object and create autograph cards of popular players such as Babe Ruth, Walter Johnson, and Honus Wagner. A brief description of this process can be found in Creager (2002) in regards to a card that features cut autographs of the first five members of the National Baseball Hall of Fame.

Although innovations occur in the industry with some regularity, it should be noted that manufacturers generally do not gain a lasting advantage from innovating. This is due to the ability of other manufacturers to quickly adjust their products by incorporating the new innovations. The mid 1990s Beckett magazines contain numerous references to this imitation. Two such references can be found in Broome (1996) and Leer (1996). The first has a quote from baseball card dealer Candy Greenholtz, “When card companies come up with new bells and whistles, others seem to follow”, while Leer’s statement came in a question and answer session among hobby dealers concerning the amount of imitation seen in the products. In an attempt to stop imitation and solidify its market position, Upper Deck filed suit to stop other manufacturers from producing cards with game-used materials embedded in them. Ultimately this lawsuit was settled out of court.30

27See O’Shei (1997a). 28See Chen (1993). 29Upper Deck had previously issued game-used memorabilia cards in 1996 hockey and football products. 30See U.S. District Court for the Eastern District of Pennsylvania (Civil Action No. 00-CV-4570).

4.1 Pricing policies 1995-2006

There has been a wide dispersion in pack prices since the early 1990s, given that different products are targeted for different consumers. As previously mentioned, Donruss released Leaf Signature in 1996 with a SRP of $9.99. While seemingly outrageous for its time, established collectors rarely balk at such prices today. Indeed, current products such as Upper Deck Ultimate Collection, Upper Deck Epic, Topps Sterling, and Bowman Sterling now carry SRPs upwards of $50 per pack of 3-5 cards and some carry SRPs into the hundreds of dollars. After 1992 it becomes difficult to compare pack prices for a few reasons. First, all the manufacturers were releasing multiple brands at this point in time.

Table of card brands and dates of manufacture

Second, the quality of the cards improved greatly, even for the basic brands, and as such comparisons with the pack prices in the 1980s become virtually meaningless. Some evidence on the increase in pack prices and price per card from 1993-1997 can be found in Keifer (1997). Although the data in the article does not adjust for quality differences, price per card increased from 13 cents in 1993 to approximately 30 cents in 1996, with the biggest increase between the 1994 and 1995 releases. The primary reason for this increase was due to the MLBPA strike in 1994, which drove borderline fans out of the hobby, leaving only diehard collectors. The demand shock also had a different effect on products of differing quality. In the basic brands there was typically a dramatic increase in the pack price while the number of cards per pack was held constant. For example, Topps increased the price of its pack by 50 cents, from 79 cents in 1994 to $1.29 in 1995 without increasing the number of cards in a pack. However, in the premium brands slight price increases tended to be accompanied by fewer cards in the pack, driving up the price per card. Another exogenous demand shock occurred in 1998, this one positive, due to the pursuit of the single season home run record.31 However, pack prices did not increase greatly. Instead, manufacturers continued to release more brands, perhaps signifying a shift in strategic behavior from price and quantity strategy to brand release strategy.

While the price per card of packs was increasing due to increasing amounts of autographs, parallel cards, serial numbered cards, die-cut cards, and laser etched cards, the introduction of the game-used cards corresponded to an even greater increase in price per pack. The process of embedding the jerseys into the cards is much more complex than changing color schemes or adding serial numbers, and the players jerseys also needed to be purchased. Once collectors warmed to the idea of game-used jersey cards, their popularity and supply increased dramatically. Most of the other changes in the industry consisted of combinations of the above changes — serial numbering game-used cards, making die-cut and parallel versions of game-used cards, having a player autograph a card that had a game-used piece embedded in it, and embedding more than one game used piece (either from the same player or different players) onto the card were some of the extensions of the previous concepts introduced. As an example of how game-used items affected price, consider the 2001 Pacific Private Stock brand. Pacific released one version of this product as a hobby-only product and another as a retail-only product. Each pack of the hobby-only product contained a game-used card and carried an SRP of $14.99 while the retail-only product did not include a game-used card and carried a $2.99 SRP.

31See Heath (1998) and Peers and Bensinger (1998).

4.2 Release Policy

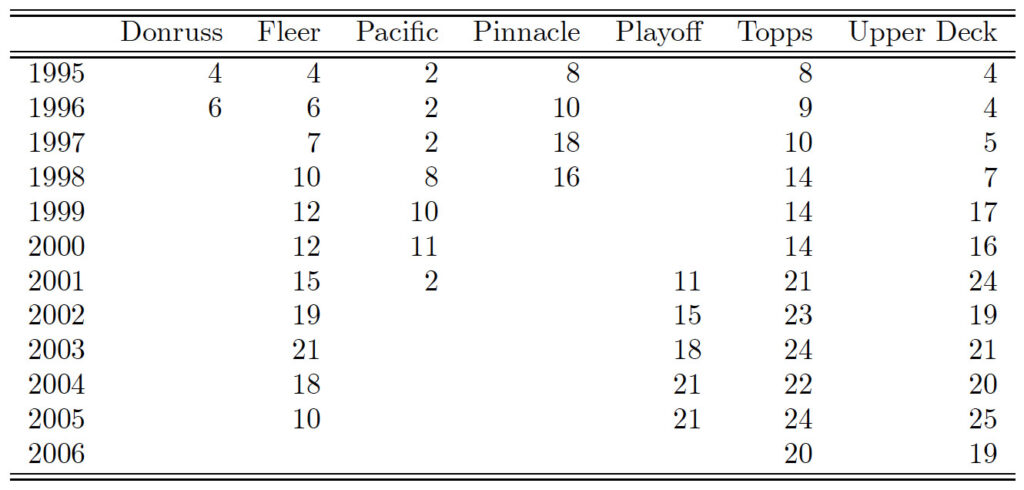

Table 2 shows the number of brands by manufacturer from 1995-2006. A few comments are in order for Table 2. The years correspond to the year as designated by the manufacturer and not the actual calendar year of the release date. The reason for this categorization is two-fold. First, actual release date for all products are not available during this time period, so the best available information is the manufacturer’s designation of the product year. Second, the brands most likely to be released in November or December of the calendar year and designated as a product for the next calendar year (e.g. 2001 Topps Series I being released in November 2000) were also the brands which were most likely to have another series issued. Since this later series would be released during the calendar year designated as the product year by the manufacturer, it would be inconsistent to consider two series of the same brand as being issued in different years. For most of the years the table covers, the process of counting brands by the calendar year designated by the manufacturer just shifts the beginning of the calendar year from January to mid-November, as once one manufacturer released a brand for the upcoming year no other manufacturers would release a brand for the current year.32 Also, although Pinnacle acquired Donruss in 1996, all brands in 1996 that were previously Donruss created (Donruss, Leaf, and Studio) as Donruss brands in 1996. Finally, after Pinnacle’s bankruptcy in 1998 and Playoff’s acquisition of the Donruss and Leaf brand names, Playoff released at least one product near the end of the 1998 calendar year, Leaf Rookies and Stars. Since Pinnacle was responsible for the design and production of Leaf Rookies and Stars it is included as a Pinnacle product.

A slight change in release strategy was triggered by Pinnacle’s bankruptcy and Playoff’s purchase of the Donruss and Leaf brand names. Due to legal action by MLB and MLBPA, Playoff was prohibited from releasing a product that Pinnacle had already produced in 1998, Leaf Rookies & Stars, until December of 1998. Because of its late release date, which was after the four current manufacturers had already released their basic 1999 products, Playoff was able to include rookie cards of some players, notably Troy Glaus and J.D. Drew, both of whom had few other cards released during 1998. About the same time, Upper Deck released a product called Upper Deck Black Diamond which contained the first Upper Deck issued J.D. Drew card and its second Troy Glaus issue. However, Upper Deck labelled the product with a 1999 date, and even though the two products were released within days of one another in December, the hobby decided that the Playoff product contained rookie cards of those players and the Upper Deck product contained 2nd year cards. Due to this designation by the hobby, the secondary market values of the cards greatly differ, and the Playoff product is heralded as one of the top products of the 1990s while the Upper Deck product is just another brand. Perhaps because of this occurrence, when Upper Deck released its Black Diamond product in 2000 it released it in two series. The second series was released in December of 2000 and was called Upper Deck Black Diamond Rookie Edition. Thus, the practice of squeezing in releases at the end of a calendar year in order to produce a few additional rookie cards began. This practice currently has limited use though as MLB and the MLBPA have recently limited who can be pictured on a rookie card.

Most of the trends in Table 2 appear to be increasing at a constant rate, with a few exceptions. The most notable exceptions are Pinnacle from 1996 to 1997, Pacific from 1997 to 1998, Topps from 1997 to 1998, and Upper Deck from 1998 to 1999. The increase in Pinnacle brands is due to its acquisition of Donruss in 1996, while the increase in Pacific brands is due to its acquisition of a full license from MLB and the MLBPA in 1998. Topps’ and Upper Deck’s increases in brands are most likely driven by the increased demand for baseball related products following the chase of Roger Maris’ single season home run record by Mark McGwire and Sammy Sosa in 1998.

There are multiple possible causes for the increase in brands. One is that due to the investor mentality of stockpiling cards in the late 1980s and early 1990s there was a glut of cards from this era still on the market once the speculators sold out. Most collectors had little use for 100 and 1000 of the same card, so in an effort to regain the sales lost by the exiting speculators, manufacturers turned to producing additional brands. The same collectors who purchased one brand could now be brought back into the market with subsequent brands, increasing sales. Thus, it is possible that collectors still wanted to purchase baseball cards but did not want to purchase the exact same cards repeatedly. In essence, collectors in general exhibited preferences for newness as defined by Krider and Weinberg (1998). Purchasing the same baseball card product is akin to a moviegoer repeatedly seeing the same movie, and while some individuals repeatedly view the same movie in the theater, most moviegoers typically view a different movie during each trip to the theater. Thus, an individual exhibits preferences for newness if that individual wishes to purchase from a general class of goods (say baseball cards or movies) but does not wish to purchase the exact same good repeatedly.

Another possible reason for the increase in brands was to solve the durable goods monopoly problem that exists in baseball cards. By producing another brand, manufacturers may have found a credible method of shortening the lifespan of a product. There is evidence that most new entrants to the baseball card market experienced this type of problem. In 1981, both Donruss and Fleer produced cards based upon collector demand. As the year progressed, if their product sold out they would print more to meet demand. After realizing that they were alienating their customers due to the adverse effects on prices in the secondary market, both Donruss and Fleer discontinued this practice in 1984. The story of 1990 Score has already been discussed earlier. There are also rumors that Upper Deck followed a similar practice of overproducing specific cards in the early years of its existence.33 While the precise reason for the shift to increasing the number of brands is unclear, it is certainly clear that the focus of manufacturers shifted from selling as much as they could of one brand to selling all they had produced of one brand as quickly as possible.

32This practice changes around 1998. See the following paragraph about the release of 1998 Leaf Rookies & Stars for more detail. 33For a detailed account of Upper Deck’s early history and policies, see Williams (1995).

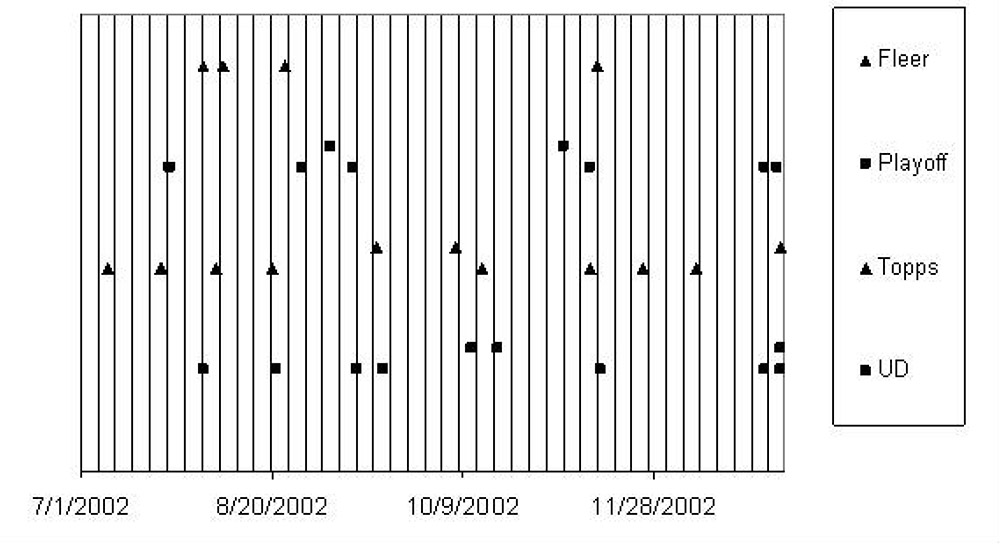

4.2.1 Release policy — A temporal Hotelling game?